![]()

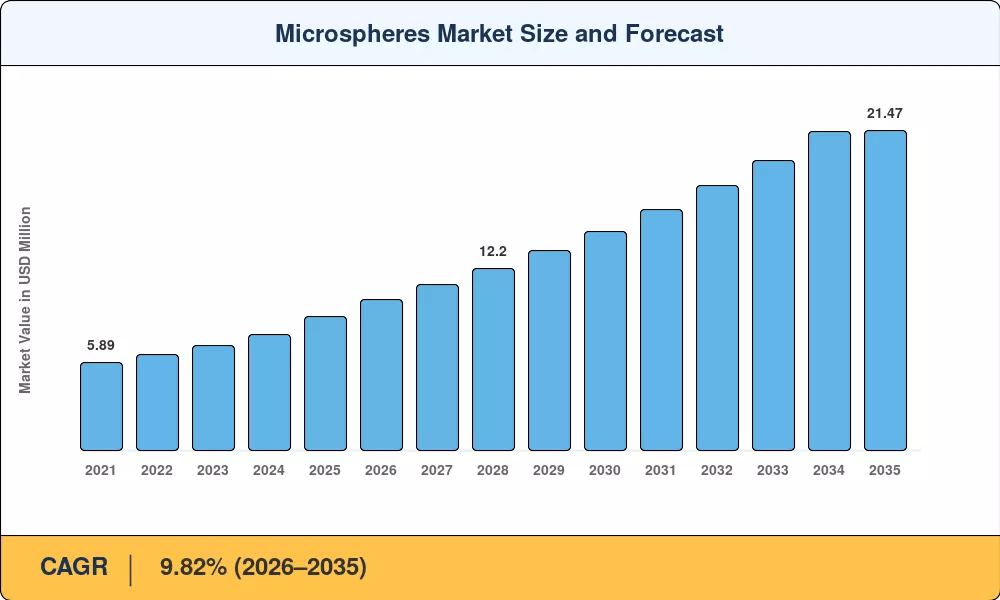

Microspheres Market to Surge from USD 10.12 Billion in 2026 to USD 21.47 Billion by 2035- By Y-90 Interventional Oncology Expansion, EV Lightweighting Mandates

NY, CA, UNITED STATES, June 15, 2026 /EINPresswire.com/ — As per Market Research Future, the global Microspheres Market size to reach USD 21.47 Billion by 2035 from USD 10.12 Billion in 2026, at a CAGR of 9.82% during the forecast period 2026–2035. The market base was estimated at USD 8.98 Billion in 2025.

The 9.82% CAGR—anchored by structural demand across medical, automotive, and industrial verticals rather than discretionary spending—is driven by three converging structural forces: the FDA’s expanding approvals for yttrium-90 glass microspheres in interventional oncology creating a premium-priced, reimbursement-supported revenue stream, global electric-vehicle production mandates in the EU, China, and the United States forcing automakers to prioritize lightweight composites where hollow glass bubbles reduce component density by up to 30%, and the pharmaceutical industry’s USD 2.4 billion combined R&D commitment to injectable microsphere formulations for long-acting drug delivery.

National governments and regulatory bodies are amplifying this momentum. The U.S. Centers for Medicare & Medicaid Services (CMS) maintain consistent coverage codes for Y-90 radioembolization procedures, lowering out-of-pocket barriers and continuously increasing clinical volumes. The EU’s stringent CO2 fleet-emission requirements aim for a 55% reduction for passenger cars by 2030 relative to 2021 baselines, equating to a target of around 42.8 g/km, directly mandating vehicle lightweighting.

China’s dual-credit policy and 14th Five-Year Plan drive EV battery enclosure material substitution. The European Commission’s REACH ban on intentionally added microplastics, enacted in late 2023, is accelerating raw-material substitution toward glass and biodegradable polymer beads across cosmetics and coatings. The Federal Highway Administration’s (FHWA) minimum pavement marking retroreflectivity requirements and Safe Streets and Roads for All (SS4A) funding programs drive demand for precision-graded solid glass microspheres. Together, these initiatives are creating the regulatory and procurement infrastructure on which engineered microspheres depend.

Request A Free Sample: https://www.marketresearchfuture.com/sample_request/2268

Key Market Trends & Growth Drivers

Interventional Oncology and Y-90 Glass Microspheres

The FDA’s approval of yttrium-90 (Y-90) glass microspheres for the treatment of hepatocellular carcinoma has created a revenue stream that is organized and supported by reimbursement. Consistent coverage codes from CMS have effectively lowered out-of-pocket barriers and continuously increased clinical procedure volumes. In March 2021, the FDA granted premarket approval (PMA) to TheraSphere Y-90 glass microspheres, expanding targeted internal radiation therapy options for liver cancer variants.

The concept that targeted drug delivery particles will support premium pricing throughout the Microspheres Market for years to come is validated by this application sector. Medical technology led the market with approximately USD 4.38 Billion in 2026 revenue, powered by radioembolization procedures and injectable microsphere formulations.

Electric-Vehicle Lightweighting and Hollow Glass Bubbles

Automakers are being forced to prioritize vehicle lightweighting by China’s dual-credit policy and the EU’s stringent CO2 fleet-emission requirements, which aim for a 55% reduction for passenger cars by 2030 relative to 2021 baselines. In battery enclosures and underbody shields, hollow glass microspheres preserve structural integrity while reducing component density by up to 30% when compared to calcium carbonate fillers.

The IEA projects global EV sales will surpass 45 million units annually by 2030, each requiring 15–25 kg of syntactic foam and composite components where hollow microspheres serve as density-reducing fillers. Major international automakers are progressively integrating these hollow microspheres into their supply chains, establishing the automotive segment as the Microspheres Market’s volume backbone alongside medical technology.

Pharmaceutical Controlled-Release Platforms and Biodegradable Polymer Beads

Injectable microsphere formulations for long-acting medication delivery—such as hormone treatments, antipsychotics, and cancer adjuvants—represent a high-growth parenteral dosage form. The number of clinical-stage drug-loaded microparticles in the regulatory pipeline has steadily increased, with the most common carrier matrix being biodegradable polymer beads (PLGA-based). The next generation of controlled-release microspheres focuses on long-acting formulations for chronic illnesses, including diabetes and metabolic management, and has already demonstrated commercial viability with the approval of leuprolide and risperidone depot microspheres.

The quickly growing GLP-1 receptor agonist class is a primary target for depot-injection reformulations, where monthly or quarterly injectable microsphere formulations would significantly improve patient adherence, creating a high-margin Microspheres Market opportunity for specialized CDMO partners with advanced PLGA encapsulation expertise.

Ask for Customization: https://www.marketresearchfuture.com/ask_for_customize/2268

Market Segment Insights

BY RAW MATERIAL

Glass: Dominant segment with ~51% share in 2026. Hollow glass bubbles for composites and targeted drug delivery particles drive demand. Borosilicate and soda-lime compositions offer tunable density and crush strength, making them the preferred filler for syntactic foams in deepwater buoyancy modules and EV structural panels. 3M’s iM series and Potters Industries reinforce market leadership.

Polymer: 8.9% CAGR (2026–2035). PLGA-based biodegradable polymer beads used in controlled-release microspheres for long-acting injectable therapies. Regulatory headwinds from ECHA’s microplastic restrictions temper expansion in non-pharma segments, pushing formulators toward biodegradable alternatives. Evonik Industries leads pharma-grade polymer microsphere production.

Ceramics: USD 0.87 Billion in 2026. High-temperature composites and electronics encapsulants drive demand. Ceramic microspheres tolerate continuous service above 1,200°C versus roughly 600°C for soda-lime glass grades, making them essential for thermal-barrier coatings in turbine components.

Fly Ash Cenospheres: ~8% share in 2026. Cost-effective construction fillers maintain a cost advantage but are losing relative share to engineered glass variants as sustainability and performance standards tighten.

Metallic & Others: Combined ~6% share. Additive manufacturing, thermal spray coatings, specialty silica, and carbon microspheres represent next-generation material frontiers.

BY TYPE

Hollow Microspheres: Dominant type with ~72% share in 2026. Benefiting from weight-reduction mandates across automotive and aerospace applications. Prized for low density, high compressive strength, and thermal insulation properties. Hollow glass bubbles reduce fluid density in oil-and-gas drilling while maintaining shear-thinning behavior critical for wellbore stability.

Solid Microspheres: 7.8% CAGR (2026–2035). Retroreflective road markings require optically precise solid glass beads, while pharma-grade solid biodegradable polymer beads function as matrix carriers for drug-loaded microparticles in depot-injection formats.

BY APPLICATION

Medical Technology: Dominant application with USD 4.38 Billion in 2026. Anchored by FDA-cleared Y-90 glass microspheres for liver-cancer radioembolization and a robust pipeline of controlled-release microspheres in Phase II/III trials. Injectable microsphere formulations for hormone treatments, antipsychotics, and cancer adjuvants represent the highest-value vertical.

Automotive: ~18% share in 2026. Catching up rapidly as hollow glass bubbles become standard bill-of-material items in EV battery enclosures and crash-structure composites. The electrification supercycle will sustain above-average demand growth through at least 2033.

Aerospace: 10.3% CAGR (2026–2035). Structural syntactic foams and thermal protection systems drive demand for high-performance hollow and ceramic microspheres.

Paints & Coatings: USD 0.92 Billion in 2026. Retroreflective markings and thermal insulation paints drive demand for precision-graded solid glass microspheres. Smart-city road safety initiatives and infrastructure safety programs expand the addressable market.

Oil & Gas: ~9% share in 2026. Drilling fluids, cementing, and completion materials consume significant volumes of hollow glass microspheres for buoyancy modules and density reduction. At 10–15% volume loading, they can lower equivalent circulating density by 1.5–2.0 ppg without degrading filtration-loss performance.

Cosmetics: 8.6% CAGR (2026–2035). Biodegradable polymer beads replacing polyethylene microbeads in personal care products, including scrubs, cosmetics, and sunscreens. ECHA’s REACH microplastic restriction mandates OECD 301-series biodegradation screening plus marine-sediment persistence testing.

Composites & Others: Combined ~8% share. Industrial syntactic foams, electronics encapsulants, and 3D printing materials represent emerging application frontiers.

Regional Outlook

North America — Dominant Market (~37% Share, 2026)

The United States generates approximately 78% of North American Microspheres Market revenue, anchored by its entrenched interventional oncology infrastructure and the world’s largest shale-drilling services sector. Medicare reimbursement expansion for Y-90 procedures and DOE-funded composite research at Oak Ridge National Laboratory continue to pull demand for both hollow glass variants and injectable microsphere formulations.

Canada is growing at 8.4% CAGR on oil-sands applications and aerospace composites. Mexico’s automotive OEM lightweighting contributes USD 0.19 Billion (2026). North America’s leadership rests on reimbursement depth, oilfield services scale, and advanced materials R&D infrastructure.

Europe — Second Largest (~26% Share, 2026)

Europe’s Microspheres Market trajectory is defined by the ECHA microplastic restriction, which is accelerating raw-material substitution toward glass and biodegradable polymer beads. Germany leads regionally with ~24% of European share, as its automotive OEMs integrate hollow microspheres into EV structural panels.

The UK is growing at 9.1% CAGR on pharmaceutical CDMO expansion and controlled-release microspheres production around Cambridge. France’s cosmetics reformulation and biodegradable polymer bead adoption contribute USD 0.38 Billion (2026). Italy’s paints and coatings sector and Spain’s infrastructure retroreflective markings at 8.7% CAGR further underpin European market depth. The Nordic countries contribute USD 0.21 Billion through green building materials. EU Horizon funding and the Corporate Sustainability Reporting Directive (CSRD) add a regulatory and ESG dimension to procurement criteria.

Asia-Pacific — Fastest-Growing Region (12.78% CAGR, 2026–2035)

Asia-Pacific is the highest-growth corridor in the Microspheres Market. China commands ~44% of regional share, with Jiangsu and Anhui glass-bubble mega-plants anchoring a regional cost advantage for automotive-grade hollow microspheres targeting domestic and international EV supply chains. India is growing at 13.2% CAGR, the fastest country-level pace, driven by the PLI scheme for advanced materials and a booming decorative-paints sector growing at 12% annually.

Japan contributes USD 0.31 Billion (2026) through aerospace composites and electronics encapsulants. South Korea’s battery enclosure materials account for ~12% of regional share. ASEAN construction fillers and cosmetics are growing at 11.8% CAGR. The region is projected to rebalance global production and consumption by the early 2030s.

Middle East & Africa — Emerging Opportunity (USD 0.41 Billion, 2026)

Saudi Arabia leads the region with ~34% of regional share, as Vision 2030 mega-projects and ARAMCO’s continued drilling investment sustain demand for hollow microspheres in oilfield services and construction composites. The UAE’s smart-city initiatives in Abu Dhabi and Dubai specify retroreflective glass microsphere coatings for road-safety compliance, growing at 9.6% CAGR.

South Africa’s mining composites contribute USD 0.05 Billion (2026). Egypt’s road infrastructure development is growing at 8.2% CAGR. The region carries the widest infrastructure gap and therefore the steepest long-term opportunity for industrial glass bead manufacturers building regional technical and distribution networks.

South America — Growing Presence (USD 0.52 Billion, 2026)

Brazil anchors South America’s Microspheres Market at ~62% of regional revenue, with pre-salt deepwater drilling operations consuming significant volumes of hollow glass microspheres for buoyancy modules and drilling-fluid weight reduction. The Ministry of Health’s hospital modernization programs provide additional construction composite demand. Argentina’s Vaca Muerta shale formation is emerging as a secondary demand driver at 8.9% CAGR. General industrial fillers and construction applications support the rest of the region.

Competitive Landscape and Recent Developments

The Microspheres Market exhibits medium concentration, with an estimated HHI below 1,200 and the top five players collectively holding approximately 38–44% of global revenue. The landscape spans diversified chemical conglomerates, specialty glass manufacturers, and pharma-focused CDMO operations, creating a multi-tier competitive structure where scale advantages in raw-material sourcing coexist with IP-driven differentiation in drug-loaded microparticles and targeted drug delivery particles.

The competitive landscape is stratified between large diversified producers controlling end-to-end glass and polymer microsphere supply chains, mid-sized specialty firms focused on precision-graded retroreflective and calibration beads, and pharma CDMOs consolidating injectable microsphere formulation capacity.

Read Detailed Insights: https://www.marketresearchfuture.com/reports/microspheres-market-2268

KEY COMPANIES AND RECENT MILESTONES

3M: Estimated revenue share ~8–11%. Broad portfolio with iM series glass bubbles and hollow microspheres for composites. Vertically integrated glass production and global distribution network reinforce market leadership across automotive, oil-and-gas, and medical verticals.

Potters Industries (PQ Group): Estimated revenue share ~5–8%. Road-safety coatings leader with retroreflective glass beads and engineered microspheres. Infrastructure focus and dual FHWA/EN 1436 certification command 10–15% price premiums in export channels.

Evonik Industries (March 2020): Expanded its Birmingham, Alabama, CDMO facility, opening a state-of-the-art facility for the formulation and GMP production of clinical-stage injectable PLGA microspheres. Estimated revenue share: ~4–6%. Pharma-controlled release microspheres leader with biodegradable polymer beads and end-to-end encapsulation, lyophilization, and fill-finish services.

Nouryon (formerly AkzoNobel Specialty): Estimated revenue share ~4–7%. Expancel expandable microspheres for thermoplastic compounding and packaging applications. Strategic positioning in lightweighting and insulation markets.

Mo-Sci Corporation: Estimated revenue share ~2–4%. Medical-technology pureplay with bioactive glass microspheres and Y-90 radiotherapy beads. FDA-cleared devices and specialized pharmaceutical-grade production capabilities differentiate from commodity producers.

Future Outlook: 2026—2035

By 2030, AI-optimized manufacturing and quality assurance will become standard across the Microspheres Market. Machine-learning algorithms applied to spray-drying and emulsion-solvent-evaporation processes will reduce particle-size variability by 30–40% within the next five years.

Real-time defect detection using computer-vision systems is already operational at two major glass microsphere plants, and pharma-grade controlled-release microspheres producers are piloting predictive-maintenance models that cut unplanned downtime by 22%. These advances will compress cost curves and lower barriers for emerging-market producers.

Platform economics in pharmaceutical microsphere CDMOs will consolidate production capacity. Contract development and manufacturing organizations specializing in injectable microsphere formulations are consolidating into platform models that offer end-to-end encapsulation, lyophilization, and fill-finish services.

Evonik, Oakwood Labs, and Phosphorex have each expanded capacity since 2023, and the top five CDMOs now control an estimated 55% of outsourced drug-loaded microparticles production. This platform-economics dynamic mirrors trends in biologics manufacturing and will concentrate Microspheres Market pharma revenue among fewer, larger operators.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/drug-delivery-system-market-43638

https://www.marketresearchfuture.com/reports/controlled-release-drug-delivery-market-6794

https://www.marketresearchfuture.com/reports/injectable-drug-delivery-devices-market-1211

https://www.marketresearchfuture.com/reports/embolization-particle-market-4815

https://www.marketresearchfuture.com/reports/nanomedicine-market-10832

https://www.marketresearchfuture.com/reports/biodegradable-polymer-market-11302

https://www.marketresearchfuture.com/reports/pharmaceutical-excipients-market-868

https://www.marketresearchfuture.com/reports/tissue-engineering-market-2134

https://www.marketresearchfuture.com/reports/regenerative-medicine-market-2220

https://www.marketresearchfuture.com/reports/biomaterial-market-2021

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery